In early 2025, the U.S. Senate introduced the GENIUS Act - short for Guiding and Establishing National Innovation for U.S. Stablecoins (Act). While its core purpose is to define a regulatory framework for payment stablecoins, the Act also introduces broader implications for institutions engaged in tokenized asset issuance and investment.

Below, we break down what the GENIUS Act actually does, what it doesn’t, and how it could shape the evolution of tokenized real-world assets (RWAs).

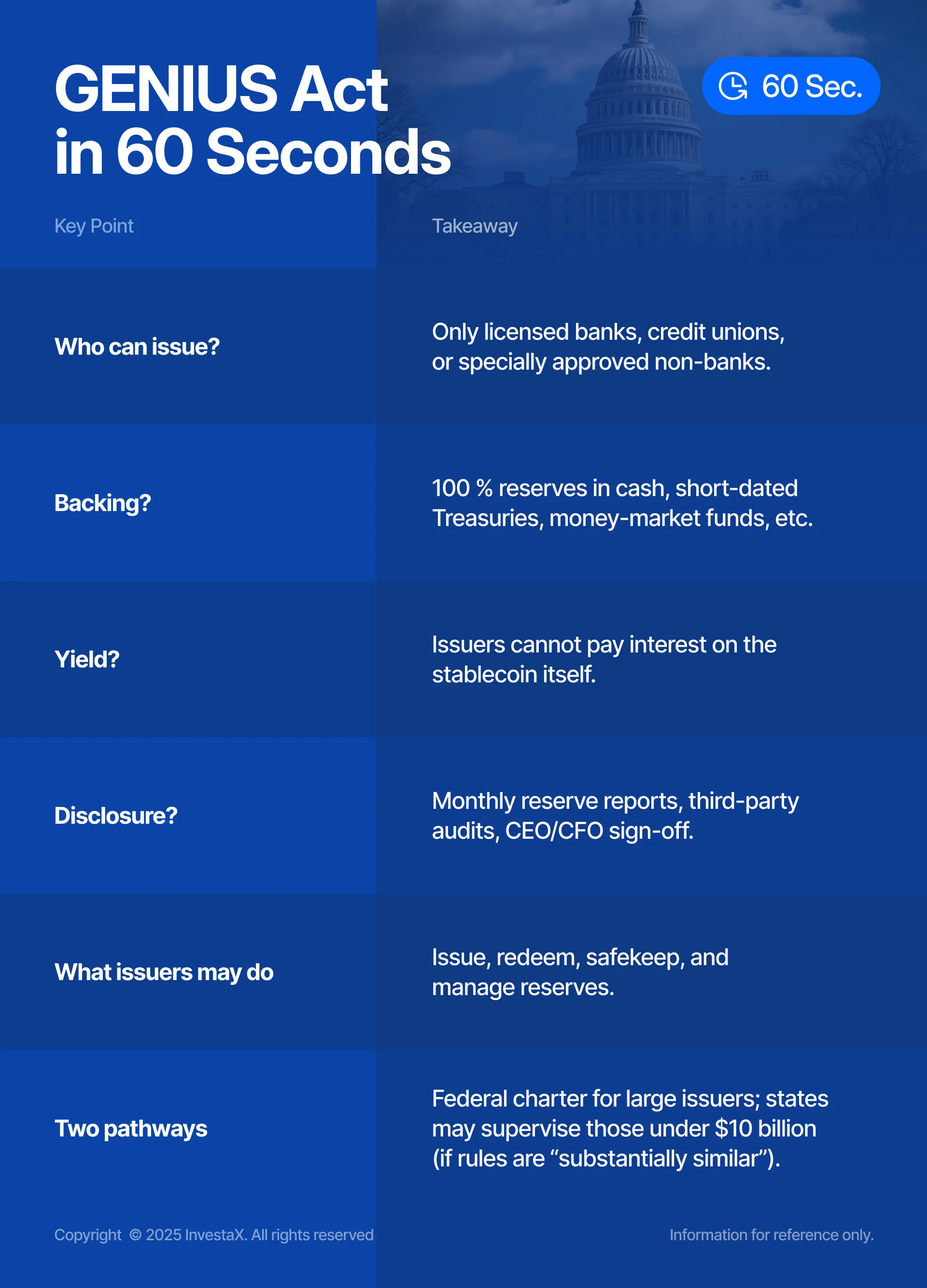

What Is the GENIUS Act?

The GENIUS Act aims to bring stablecoin issuance under federal oversight, defining clear requirements for what constitutes a compliant, U.S.-issued payment stablecoin.

At a high level, it limits who can issue stablecoins, how they must be backed, what they can (and cannot) do with reserves, and how those reserves are disclosed.

While the Act does not regulate tokenized securities or tokenized RWAs directly, it formalizes the infrastructure many tokenized products depend on, including regulated stablecoins used for payments, subscriptions, redemptions, and settlement.

What This Could Mean for RWA Tokenization?

While the GENIUS Act doesn’t directly regulate tokenized RWAs, its effects could ripple across the ecosystem in several key ways. So, what are the potential impacts of the GENIUS Act on real-world asset tokenization?

1. Stablecoin Growth & Yield Migration

What may change?

- Clear rules could make it easier for corporates and funds to park working capital in stablecoins.

- Because issuers can’t pay interest, large holders will look elsewhere for returns.

With the GENIUS Act providing regulatory clarity, the stablecoin market, currently valued around $250 billion has room to grow as more issuers enter the space. But because the Act prohibits stablecoin issuers from paying interest, institutional holders seeking returns will need to deploy capital into other yield-generating strategies like RWAs.

Where the yield may go?

Tokenized fixed income products, such as money market funds (MMFs), corporate bonds, and Treasuries, can help meet that need. These instruments not only offer regulated returns but can also function as on-chain collateral, increasing their utility.

Bottom line: Clearer rules can grow the stablecoin pool while pushing yield off the coin itself, directing that fresh capital toward regulated, yield-bearing RWAs.

2. More Demand for Stablecoin-Denominated Structures

We expect demand to increase for tokenized investment products that accept or are denominated in stablecoins. Examples of such stablecoin-compatible RWA models include:

- Tokenized notes or feeder funds that accept GENIUS-compliant coins by default.

- On-chain MMF clones offering same-day liquidity and daily accrual.

- Secondary markets quoting in stablecoin pairs, reducing the need for off-chain cash buffers.

Examples include InvestaX MMF Earn and Tokenized HYCB, which enable stablecoin holders to earn 4-8% APY from underlying assets like BlackRock’s $6.4B ETF and Fidelity’s USD money market fund. Yields accrue daily, and investors retain opt-in and opt-out flexibility.

Also read: GENIUS Act and The Rise of Tokenized Yields

3. Stablecoins as a Payment Method for Tokenized Securities

Until now, institutions have largely avoided accepting stablecoins for tokenized security transactions due to regulatory and accounting concerns like SAB 121. This has slowed progress toward atomic on-chain settlement, where assets and payments settle together.

The GENIUS Act introduces the potential to change that by introducing a compliant framework for issuing and using fully backed payment stablecoins. Institutions may now feel more comfortable using stablecoins for subscription, redemption, and settlement of tokenized securities, reducing friction and delays.

4. (Longer-Term) Tokenization of Reserve Assets

Stablecoin issuers must back coins with liquid assets like MMFs and Treasuries. To provide full transparency and auditability, those assets may themselves become tokenized. This could effectively expand the tokenized asset universe, although this remains a developing area.

What Institutions Should Watch

- Stablecoin onboarding frameworks: Ensure tokenized products are designed to accept stablecoins for subscriptions, redemptions, and collateral.

- Accounting treatment: The Act’s clarity may support more favorable booking than current guidance (e.g., SAB 121). Speak with auditors early.

- Investor communication: Institutional investors may increasingly demand clarity on how stablecoins are used within RWA structures.

- Cross-border considerations: The Act allows for reciprocity with overseas stablecoin regimes, which could affect how tokenized securities are distributed globally.

Final Thoughts

The GENIUS Act doesn’t touch RWAs directly, but it tidies up the cash rails they depend on. If stablecoins scale into the trillions, as some analysts believe, those coins will need productive, regulated homes. Tokenized fixed-income products are well-positioned to provide that outlet.

For issuers and platforms, the takeaway is simple: design with stablecoin compatibility in mind, keep disclosures tight, and be ready for faster settlement expectations. The plumbing is falling into place; the next wave of on-chain assets could move through it quickly.

Have questions? Reach out to the InvestaX team to discuss your tokenization strategy.